7 Best Cash Advance Apps To Help You Out Until Payday

Cash advance apps let you access a portion of an upcoming paycheck before it arrives. If you’re struggling to pay bills or have an emergency expense, these apps can help make ends meet until payday. Plus, they’re often cheaper than turning to a credit card or personal loan.

However, there are dozens of cash advance apps out there. Some of them have higher fees or different advance limits you should be aware of. That’s why our team has compiled a list of the top apps you can use as well as some other alternatives.

Best Cash Advance Apps - Quick Summary

| Cash Advance App | Advance Amount | Deposit Time | Instant Cash Fee | Other Fees |

|---|---|---|---|---|

| EarnIn | $100 to $750 | 1 - 3 days | $3.99 - $4.99 | No |

| Dave | Up to $500 | 1 - 3 days | $3 - $25 | $1 monthly membership |

| Chime | Up to $500 | 1 - 3 days | $2 | No |

| Klover | $5 to $200 | 3 days | $1.50 - $20.78 | $3.99 monthly Klover+ fee |

| Brigit | $50 to $250 | 1 - 3 days | $0.99 - $3.99 | $8.99 or $14.99 monthly membership |

| Empower | $10 to $250 | Instant | $1 - $8 | $8 monthly membership |

| MoneyLion | Up to $1,000 | 1 - 5 days | $0.49 - $8.99 | No |

EarnIn: Best for Large Advances

![]()

EarnIn is Homeowner’s number one pick for the top cash advance apps. And the main reason for this is that it lets you access up to $750 per pay period; the highest limit out of any app on our list.

👍

Pros

- Borrow up to $750

- Pay-what-you-want tip model

- Low Lightning Speed fee

- Get a free credit score

👎

Cons

- Can only borrow $100 per day

- Users don’t always qualify for cash advances

Highlights

Cash Advance Limit: Up to $750 per pay period

Best For: Large advances

Advance Deposit Time: 1 to 3 days

Fast-Advance Fee: $3.99 to $4.99

Other Fees: Option tips up to $13

Repayments: Withdrawn automatically on your next payday

Apple App Store Rating: 4.7 stars

Google Play Rating: 5 stars

Pricing & How EarnIn Works

EarnIn uses a “pay what’s fair model” where you choose how much to tip after taking out an advance. You can tip up to $13 per advance or choose to pay $0. There’s no membership fee, which is another selling point.

Cash advances from EarnIn usually arrive within one to three business days. Alternatively, you can pay an express fee of $3.99 to $4.99 to receive your money almost instantly with its Lightning Speed feature.

Like other leading cash advance apps, EarnIn doesn’t charge interest. It doesn’t run a soft or hard credit check either. Plus, you can get a free credit score from Experian as an EarnIn user.

Read the full EarnIn review >>

Dave: Best for Easy Repayments

![]()

Daveis another leading cash advance app that has over 6 million members. It lets you borrow up to $500 with its ExtraCash feature.

Like EarnIn and other apps, you don’t pay interest, late fees, or go through a credit check. And Dave has some of the easiest repayment terms in the entire business.

👍

Pros

- High cash advance limit

- Easy repayment terms

- Helps you find new side hustles

- Low monthly membership cost

👎

Cons

- Instant cash deposit fees are high

- No free plan

Highlights

Cash Advance Limit: Up to $500

Best For: Easy repayment terms

Advance Deposit Time: 1 to 3 business days

Fast-Advance Fee: $3 to $25

Other Fees: $1 monthly membership fee

Repayments: Withdrawn automatically on your next payday

Apple App Store Rating: 4.8 stars

Google Play Rating: 4.5 stars

Pricing & How Dave Works

Like other cash advance apps, you connect your bank account to Dave to qualify for your cash advance limit. You can borrow up to $500 per pay period. However, you have to pay a $1 monthly membership fee to use the ExtraCash feature.

Fast-funding fees can get a bit steep depending on how large your advance is. This is why we recommend giving yourself enough time on your advance so you can get one for free.

We also like Dave since it has tons of other features. There’s a tool to help you find new money-making opportunities and side hustles. Dave also has a goals account that pays 4.00% APY. Overall, it’s more robust than your average cash advance app, which is why it’s #2 on our list.

Read the full Dave review >>

Klover: Best for Beginners

![]()

Klover is a free money app that lets you borrow $5 to $200 between paydays. And it’s one of our favorite apps if you’re struggling to get high approval amounts with some of Klover’s competitors.

That’s because Klover lets you complete various tasks to increase your cash advance limit. For example, you can answer surveys or watch videos to gradually increase your limit. In contrast, most apps just connect to your bank account to determine your limit.

👍

Pros

- Numerous ways to increase your cash advance limit

- Klover runs daily cash sweepstakes

- A more “fun” app than its competitors

- Useful if you have limited paycheck history

👎

Cons

- Lower cash advance limit than many competitors

- Instant cash deposit fees are high

- Klover+ is expensive for the budgeting tools you get

Highlights

Cash Advance Limit: Up to $200 per pay period

Best For: People with little payment history

Advance Deposit Time: 3 business days

Fast-Advance Fee: $1.50 to $20.78

Other Fees: Option tips; $3.99 per month for Klover+

Repayments: Withdrawn automatically on your next payday

Apple App Store Rating: 4.7 stars

Google Play Rating: 4.6 stars

Pricing & How Klover Works

Klover connects to your bank account to determine your limit like other cash advance apps. But you can complete a variety of tasks to slowly increase your limit, which is a unique selling point.

We also like that Klover has daily cash sweepstakes and makes things a bit more exciting versus similar apps. You can even access budgeting tools and credit score tracking if you upgrade to a Klover+ plan. However, Klover+ costs $3.99 per month, and we recommend other standalone budgeting apps like Rocket Money or YNAB instead.

But for easy cash advances, especially when starting out your payment history, Klover is worth trying.

Read the full Klover review >>

Brigit: Best for Building Credit & Budgeting

![]()

Brigit is yet another cash advance app that’s similar to Dave and EarnIn. It lets you borrow up to $250 in a pay period with its Instant Cash feature. There’s no tip or fee, but you need to pay for a Brigit plan to unlock cash advances.

Brigit Plus starts at $8.99 per month. This unlocks cash advances plus plenty of other features like credit score monitoring, identity theft protection, a side hustle finder tool, and pretty decent budgeting tools to help you save more money. You can also upgrade to Brigit Premium for $14.99 per month to access Brigit’s credit-builder tool.

👍

Pros

- Has useful budgeting tools

- Also helps you build your credit

- Simple pricing structure

- Brigit Premium members get some discounts

👎

Cons

- Expensive monthly membership plans

- Low cash advance limit versus some competitors

- Must be active for 60 days on Brigit before taking out an advance

Highlights

Cash Advance Limit: Up to $250 per pay period

Best For: Building credit and budgeting

Advance Deposit Time: 1 to 3 days

Fast-Advance Fee: $0.99 to $3.99

Other Fees: $8.99 or $14.99 monthly subscription fee

Repayments: Withdrawn automatically on your next payday

Apple App Store Rating: 4.8 stars

Google Play Rating: 4.7 stars

Pricing & How Brigit Works

You have to pay for a Brigit plan to take out a cash advance. But you don’t have to worry about tips or hidden charges on your advance. And what makes Brigit unique is how many tools you get alongside the ability to take out an advance.

For example, Brigit’s budgeting tools let you examine your monthly spending habits and patterns. You can also get reminders about upcoming bills and forecast how much you’re spending in a month. Plus, Brigit has a useful Earn & Save product that helps you find side hustles and new income opportunities.

On top of that, Brigit’s Credit Builder account helps you begin improving your credit starting at only $1 per month. If you’re looking for a cash advance app and some credit or budgeting help, Brigit could be for you.

That said, if you’re only looking for free cash advances, we suggest using apps like EarnIn.

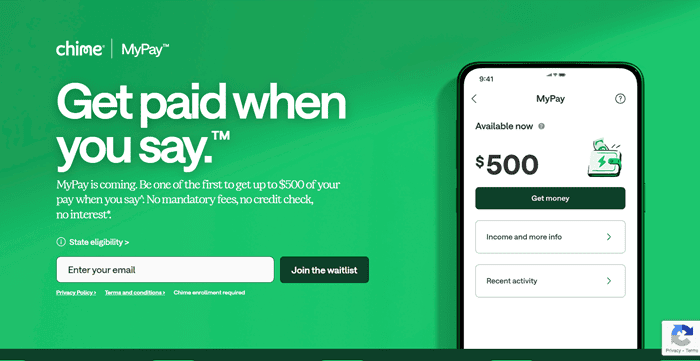

Chime: Best for Low Fees

![]()

Chime is a popular FinTech company that’s best known for its lack of fees. It also has plenty of features to help you save money and get access to your money much faster.

For starters, Chime provides up to $200 in fee-free overdraft with its SpotMe feature. And it’s now rolling out a new cash advance feature, Chime MyPay, which lets users borrow up to $500 in a given pay period.

There are other nifty features, too. You can get paid up to two days early if you set up direct deposit. And Chime also has a nifty credit-building product, too.

👍

Pros

- Lack of fees

- Low instant cash advance fees

- Up to $200 in overdraft protection

- Other useful banking features

- Often has referral bonuses

👎

Cons

- Chime MyPay is still rolling out to customers

- You have to be a Chime customer to use its new cash advance feature

Highlights

Cash Advance Limit: Up to $500

Best For: Other banking features

Advance Deposit Time: 1 to 3 days

Fast-Advance Fee: $2

Other Fees: No

Repayments: Withdrawn automatically on your next payday

Apple App Store Rating: 4.8 stars

Google Play Rating: 4.5 stars

Pricing & How Chime Works

Chime has always been know as one of the best fee-free banking solutions. It’s extending this practice to cash advances via its MyPay feature. You can get an advance for free if you wait a few business days. Otherwise, Chime charges a flat $2 instant advance fee.

This fee is one of the lowest in the entire industry. You don’t get asked for tips either, and Chime doesn’t charge interest or impact your credit score. Plus, you can use its SpotMe feature for up to $200 in fee-free overdrafts while you wait for MyPay approval.

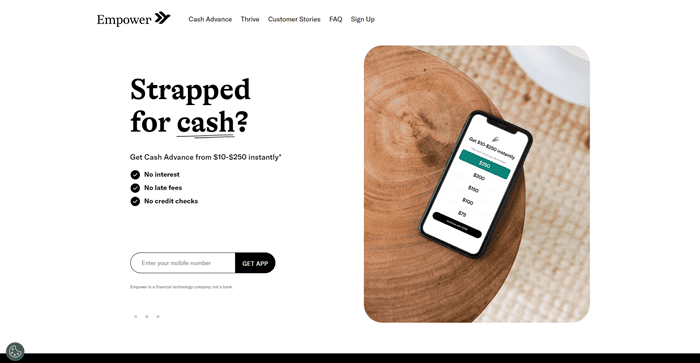

Empower: Best for Instant Cash Advances

![]()

With Empower, you can get $10 to $250 in a cash advance per pay period. And like the other top apps in this space, there are no credit checks, late fees, or interest charges to worry about.

The platform also has a host of other features similar to apps like Brigit. You can use its Empower Thrive line of credit to begin improving your credit score. The app also has automatic savings features and a spend tracker tool to help you spend less money.

👍

Pros

- Offers instant cash advances

- Has a credit-building tool

- Also offers budgeting help

- Has a 14-day free trial

👎

Cons

- Low cash advance limit versus some competitors

- Expensive monthly membership

Highlights

Cash Advance Limit: $10 to $250 per pay period

Best For: Instant cash advances

Advance Deposit Time: Instant

Fast-Advance Fee: Optional $1 to $8 tip

Other Fees: $8 monthly membership fee

Repayments: Withdrawn automatically on your next payday

Apple App Store Rating: 4.8 stars

Google Play Rating: 4.7 stars

Pricing & How Empower Works

What sets Empower apart from other cash and loan apps is that most customers who qualify for an advance get their money instantly. For Empower, this means within 15 minutes on average.

You don’t have to pay fast advance fees, although Empower asks for a $1 to $8 fee and up to 20% in tips per advance. But you’re not obligated to pay anything since you’re already paying $8 per month.

As mentioned, Empower also has plenty of other features. It can be a good choice if you want instant cash advances but also need some budgeting help. However, we think Brigit is a more robust app than Empower when it comes to budgeting and credit building.

That said, Empower is one of the best options if you’re tired of fast advance fees and are okay with paying $8 per month.

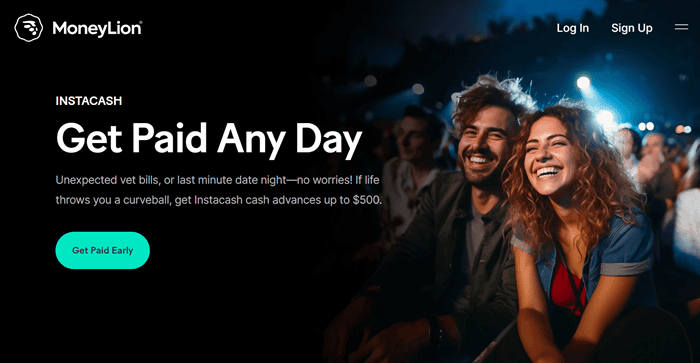

MoneyLion: Best for Banking & Investing Features

![]()

MoneyLion isn’t just a cash advance app. Rather, it’s a banking solution with a host of features. One of these is MoneyLion’s Instacash cash advance feature that lets you borrow up to $500 per pay period.

There are no interest, credit checks, or mandatory fees like other leading apps. And if you bank with MoneyLion through its MoneyRoar program, you can actually increase your advance limit up to $1,000.

👍

Pros

- Tons of banking and investing features

- Customers can increase cash advance limit up to $1,000

- Has a credit-building tool

👎

Cons

- Best for existing MoneyLion customers

- Instant cash advance fees can be high depending on amount

Highlights

Cash Advance Limit: Up to $500 per pay period

Best For: Banking and investing features

Advance Deposit Time: 1 to 5 business days

Fast-Advance Fee: $0.49 to $8.99

Other Fees: Optional tips

Repayments: Withdrawn automatically on your next payday

Apple App Store Rating: 4.7 stars

Google Play Rating: 4.5 stars

Pricing & How MoneyLion Works

You don’t need a MoneyLion bank account to use its Instacash feature. However, MoneyLion MoneyRoar members get discounts on instant cash delivery. Members can also increase their advance limit up to $1,000 per pay period with qualifying direct deposits. This is one of the highest advance limits in the space and is certainly a selling point for MoneyLion customers.

The platform has tons of other products too. For example, you can use its managed investing service or even invest in crypto. There’s also a credit-building tool similar to apps like Brigit and Empower. Plus, MoneyLion has plenty of loans and credit cards it recommends to members based on their goals and financial history.

If you’re a current MoneyLion customer, this is definitely the best cash advance company you can use. But we think apps like Dave and EarnIn might be better choices if you’re not looking for a new banking solution right now.

Read the full MoneyLion review >>

How To Choose the Best Cash Advance App

At Homeowner, we considered over a dozen loan apps and cash advance solutions for this guide. There are certainly more companies out there you can consider. However, we believe the companies above are the top choices.

Here are some of the main features we considered when ranking these apps, as well as some factors you should consider:

- Cash Advance Limits: How much money do you need to borrow until your next paycheck? Generally, $500 is the most you can borrow with most leading cash advance apps.

- Fees: Consider membership fees, instant-advance fees, and optional tips when making your decision.

- Annual Percentage Rate (APR): APR represents the interest rate you pay on a loan for a whole year. It’s always worth considering what the APR of a cash advance is, even if you’re paying it back quickly. Between tips and instant deposit fees, some cash advances can have horrendously high APRs and are not always a wise choice.

- Advance Times: Most leading apps deposit cash advances for free within three business days. This is important since you want to avoid instant-advance fees whenever possible.

- Other Notable Features: Some apps offer budgeting tools, credit-building accounts, banking features, and even side hustle finders. Think about what else you want in an app before making your choice.

[starbox color=lightblue] The Bottom Line: At Homeowner, we don’t think cash advance apps should be something you use every week. These apps can help you out in a sticky situation but shouldn’t be relied on since they can create a pattern of constant borrowing.

[/starbox]

The Best Alternatives To Cash Advance Apps

If you need money quickly, you can use apps like EarnIn, Dave, Empower, and others mentioned in this guide. However, there are also other alternatives worth considering before you use one of these apps:

Some popular alternatives to using cash advance apps include:

- Asking friends or family to spot you some cash

- Starting an in-person or online side hustle to make more money

- Using your credit card

- Considering a personal loan

- Using a buy-now-pay-later (BNPL) solution like Klarna or Affirm

Ultimately, the goal is to not get in the habit of borrowing money and living paycheck to paycheck. But if times are tough or emergencies strike, there are options you can use for fast funding.

Wrapping Up: Are Cash Advance Apps Right For You?

Cash advance apps aren’t for everyone. The ideal user is someone who normally has enough money to make it between paychecks but needs a helping hand to cover some extra bills. If you don’t have a stable paycheck or are already struggling with debt, we don’t recommend using these apps.

That said, cash advance apps have much lower fees than payday loans or many personal loans. If used responsibly, they can help cover emergencies without painful interest charges and late fees.